Categories

Home Buying TipsPublished May 11, 2026

How Property Taxes Affect Your Monthly Mortgage Payment?

If you’ve started looking at homes online or touring properties, you may have noticed something confusing: Two homes with similar prices can have very different monthly payments.

That difference often comes down to one overlooked factor; property taxes. At first glance, they might seem equally affordable, but the numbers can shift quickly once taxes are factored in.

This is one of the most common surprises buyers encounter as they transition from general budgeting to comparing actual homes.

As real estate professionals, we often see this; buyers focusing on purchase price, only to realize later that location-driven costs such as property taxes can significantly alter what a home actually costs each month.

In this article, we’ll break down how property taxes impact your monthly payment, why they vary so much depending on where you’re looking, and how to think about these differences as you start evaluating homes, so you can avoid budget surprises and make more confident decisions.

What Makes Up a Monthly Mortgage Payment?

When you start comparing homes, it’s easy to focus on the listing price, but your monthly payment is made up of several components, and not all of them stay the same from one property to another.

A typical monthly mortgage payment includes:

- Principal & Interest (the portion that goes toward paying off your loan)

- Property taxes (the payment to the local municipality based on the assessed value of the property)

- Homeowners insurance

- Mortgage Insurance (if you put less than 20% down)

While principal and interest are largely driven by your loan amount and interest rate, property taxes can vary significantly depending on the location of the home.

Why Property Taxes Can Dramatically Change Your Monthly Payment

Property taxes aren’t a small add-on; they can meaningfully impact what you pay every month.

Let’s look at a simple example:

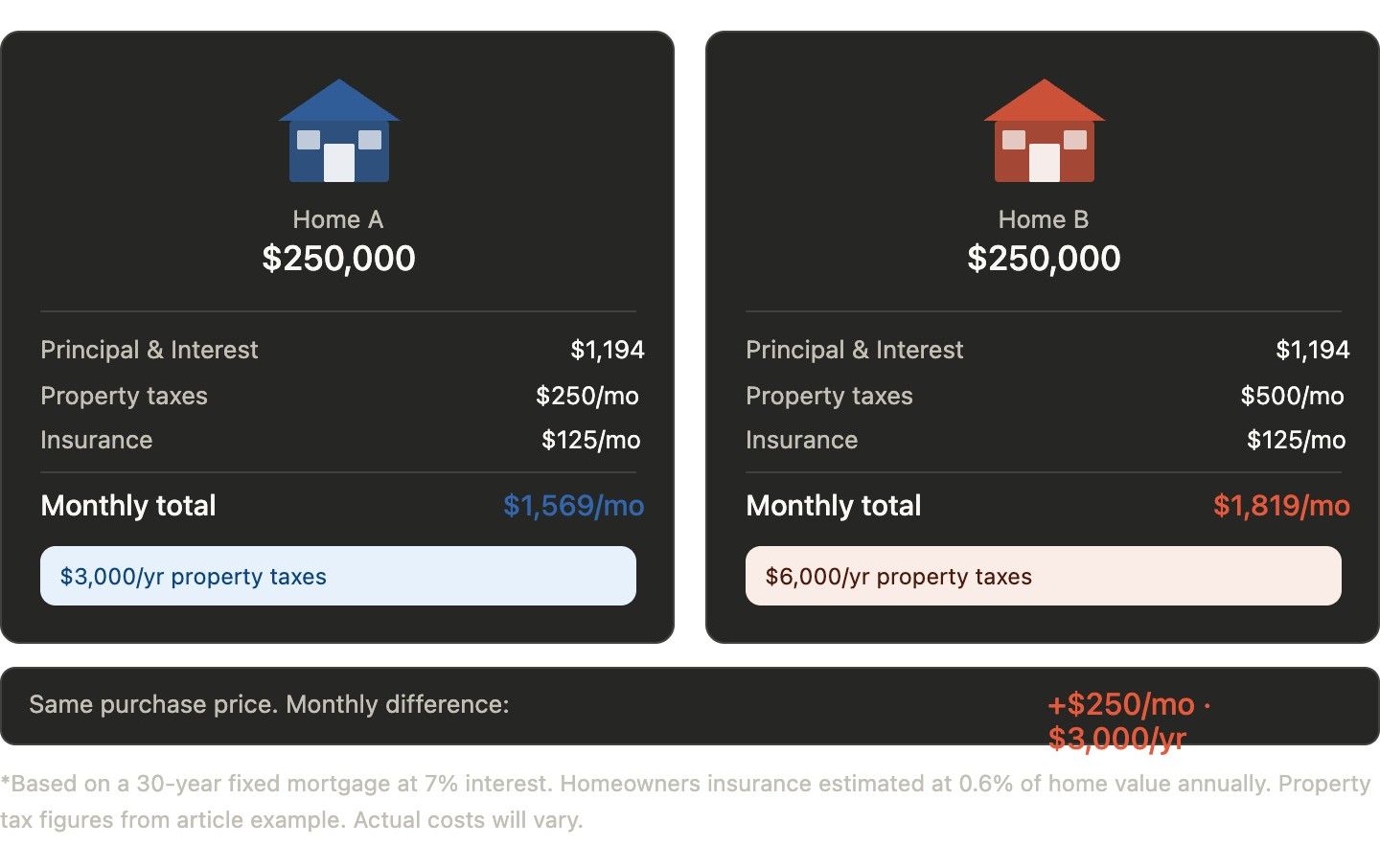

Imagine you’re comparing two $250,000 homes.

- One has $3,000/year in property taxes.

- The other has $6,000/year.

That’s a $3,000 annual difference, or about $250 more per month.

In other words, a home that looks “cheaper” on paper can actually cost you more each month.

This is why property taxes are often overlooked but critically important when budgeting.

Why Property Taxes Vary So Much (Even Nearby)

One of the most confusing parts for buyers is how much property taxes can vary, even between homes that are close to each other.

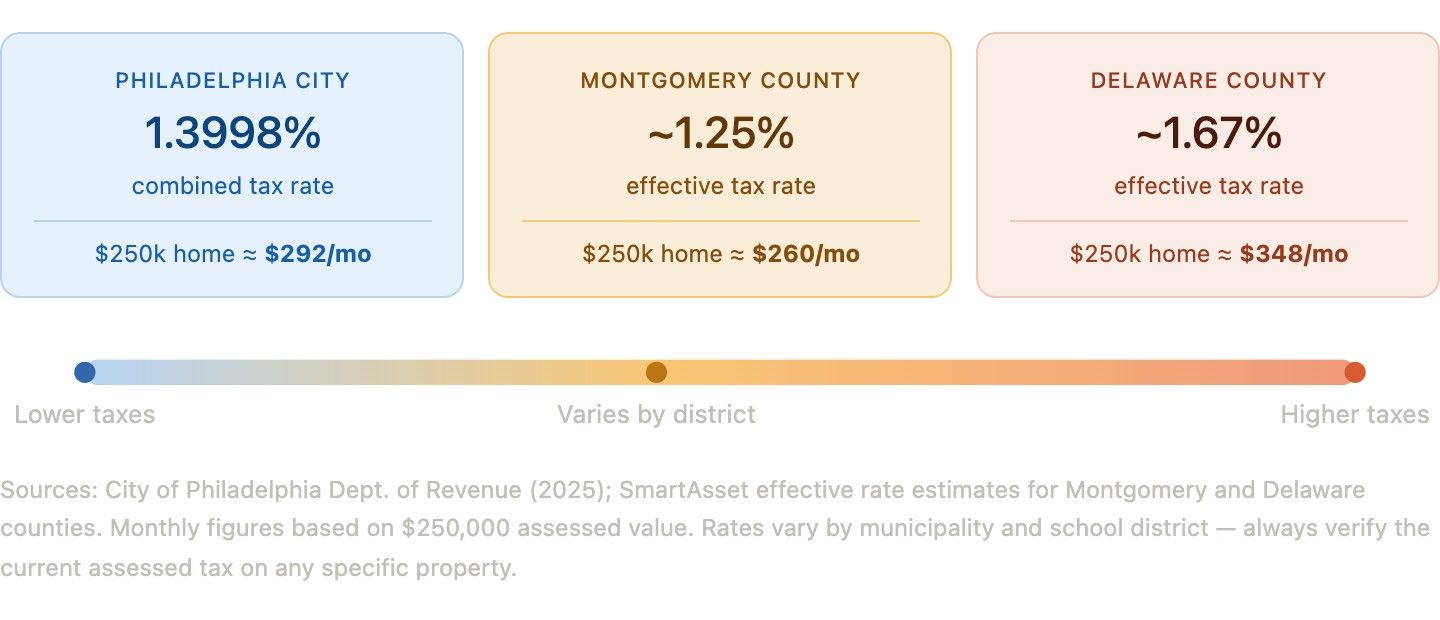

Property taxes vary by location, largely based on school districts and local municipal services (according to the Tax Foundation). Even nearby homes can fall into different tax areas, which can significantly change your monthly payment.

That’s why you’ll often see:

- Lower property taxes in Philadelphia

- Higher property taxes in suburban counties like Montgomery or Delaware counties

How Property Taxes Are Paid Through Your Mortgage

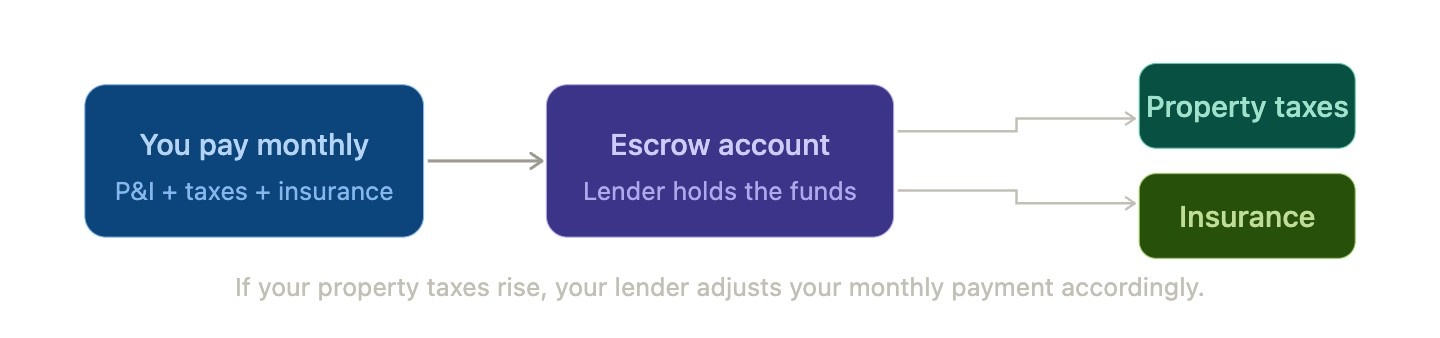

Most homeowners don’t pay property taxes separately; instead, they’re included in your monthly payment through something called an escrow account.

Here’s how it works:

- A portion of your monthly payment goes into escrow.

- Your lender holds those funds.

- They pay your property taxes and insurance on your behalf.

This makes things easier, but it also means your monthly payment isn’t completely fixed.

Many buyers assume their payment will stay the same, but that’s not always the case. If your property taxes increase, your monthly payment will increase too.

How to Accurately Estimate Your Monthly Payment

As real estate professionals, we often see this; buyers focusing on the purchase price only to realize later that location driven costs such as property taxes can significantly alter what a home actually costs each month..

The best way to avoid surprises is to look beyond rough estimates and start thinking about the full monthly cost, especially as you begin comparing homes.

You don’t need exact numbers yet, but you do need a clearer picture than most online tools provide.

As you evaluate different homes, here’s how to get a more realistic estimate:

- Look up the property’s current tax amount.

This is often publicly available and gives you a much better starting point than a generic estimate. - Compare homes across different areas.

If you’re looking in multiple towns or school districts, expect property taxes and monthly payments to vary. - Factor in all components of the payment.

This includes taxes, insurance, and (if applicable) PMI, not just principal and interest. - Use online estimates as a starting point, not a final number.

They can help you get in the ballpark, but shouldn’t be the number you rely on when making decisions.

As you get closer to narrowing down your options, your agent or lender can help you refine these numbers further.

But even early on, taking these extra steps can give you a much clearer understanding of what you can comfortably afford, and which homes truly fit your budget.

What to Do as You Start Comparing Homes

As you begin looking at specific homes, don’t rely on purchase price alone to guide your budget.

Property taxes play a major role in what you’ll actually pay each month, especially when comparing homes across different areas.

This is one of the most common areas where buyers get tripped up, so if it feels confusing, you’re not alone.

As you evaluate your options, pay close attention to how taxes vary from one property to another, and treat online estimates as a starting point, not a final number.

The buyers who avoid budget surprises are usually the ones who asked the right questions early. If you want help running the real numbers on a home you're considering, send us a message, just share the address and we'll walk you through the full monthly cost.

|

or another way