Categories

Home Buying TipsPublished April 1, 2026

How to Write a Competitive Home Offer: Why It’s More Than Just the Price

If you're buying a home, especially in a competitive market like Greater Philadelphia, you’ve probably been told how important it is to “write a strong offer.” But what does that actually mean? Too often, buyers assume it’s just about picking a price and signing paperwork. In reality, your offer is a complex mix of deadlines, legal terms, and financial decisions and getting this wrong could mean losing your offer on your dream home.

Our team has written over a thousand offers, and helped hundreds of buyers win, by making sure they understand how the offer actually works before they’re in a bidding war or emotionally invested in a home.

In this article, we’ll break down the five key elements of a strong home offer; price, earnest money, inspections, financing, and timing, so you can make confident, strategic decisions on the terms of the offer your agent will write for you.

What Makes a Competitive Offer on a House? 5 Key Elements Buyers Must Understand

While contracts can feel overwhelming, most offers boil down to five major components:

- Purchase Price

- Earnest Money Deposit

- Inspections

- Financing

- Closing Date

When buyers learn the nuance of each of these elements individually, the offer stops feeling intimidating—and starts feeling strategic.

The Role Purchase Price Plays In Your Home Offer

Let’s start with Price. The Purchase Price is important to a competitive offer, but it’s rarely the whole story.

What Does the Purchase Price Number Really Mean?

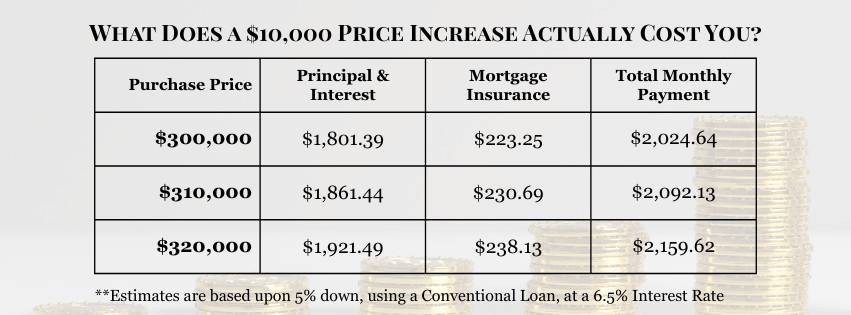

One common mistake buyers make is focusing on the headline number without understanding how it affects their actual finances. A $300,000 offer sounds concrete, but what matters more is how that number impacts monthly payment and cash to close.

A helpful way to frame this is in increments. Roughly speaking, every $10,000 in purchase price often translates to about $60–$70 per month, depending on interest rates. For many buyers, that realization changes the conversation entirely. A hard line at $310,000 can soften quickly once they see it’s the difference of a few dollars a day—not tens of thousands upfront.

Down payment structure matters too. With a low down payment, that same $10,000 difference might only mean a few hundred dollars more at closing. Seeing the numbers laid out clearly helps buyers decide what they’re truly comfortable with—before emotions take over in a competitive situation.

This is why reviewing an estimated cost sheet with your agent before deciding on the terms of an offer is essential. It turns an abstract price into a real, livable decision.

Why Can the Asking Price Be Misleading? (Market Value vs. List Price)

List price is a marketing tool.

Some sellers intentionally price low to generate multiple offers. Others overshoot and expect negotiation. That’s why strong offers are grounded in comparable sales, not just the number on the listing.

Looking at recent, nearby sales with similar size, condition, and features gives agents and buyers a realistic sense of where value actually lands. In competitive markets, this matters even more. Buyers often ask, “Why would I offer more than asking?”—but when demand is high, asking price becomes irrelevant. The market, not the list price, sets the tone. That’s where an escalation clause can come in, to help protect you in these situations.

How can I protect myself by using an Escalation Clause?

You’ve just toured a home in Ardmore that checks every box—and your agent tells you it already has three offers on the table.

You don’t want to overpay, but you also really don’t want to lose your dream home. That’s when your agent brings up a smart tool: the escalation clause..

Think of it like bidding on eBay: you set a maximum you’re comfortable with, and the contract automatically increases your offer in small steps (often $3,000–$5,000) only if another buyer forces you there.

That’s especially helpful in places like Pennsylvania, where you usually don’t know what the other offers are—agents rarely disclose exact numbers—so escalation gives you a way to stay competitive without blindly overpaying.

For example, you might offer $300,000 with an escalation up to $325,000; if the highest competing offer is $305,000, you only escalate to $310,000 (or whatever the increment requires) rather than jumping straight to your max.

The key is timing: if you escalate when there are no other offers, you may tip your hand by showing the seller what you’re willing to pay, which can invite pressure or encourage them to wait for someone else to push you higher.

Let’s illustrate this! In a multiple offer situation, two buyers both offer $300,000, and use an escalation clause.

Buyer 1 escalates by $5000 up to $320,000

Buyer 2 escalates by $5000 up to $315,000

Buyer 1 escalates by $5000 to $320,000, and wins the offer

.jpeg)

How Can I Use Seller Assist wisely in my Home Offer?

Let’s say you’ve found your dream rowhome in West Philly, listed at $300,000—but after running the numbers, you realize closing costs would wipe out your emergency fund.

That’s where seller assist can make a big difference. Instead of covering all your closing costs out-of-pocket, your agent can help you to structure the offer to ask the seller to pay part of your closing costs. For example, if you need $25,000 to close and the seller agrees to a $10,000 assist, you only need to bring $15,000 to the table.

That can make a big difference, especially for first-time buyers.

What’s important to understand is that the seller assist comes out of the seller’s proceeds. If a home is listed at $300,000 and you offer $300,000 with a $10,000 seller assist, the seller is really only netting $290,000. If you want them to walk away with their full asking price, you may need to raise your offer to $310,000 and include the assist.

The home still has to appraise at its value, and the assist doesn’t magically raise that number. In competitive situations, asking for seller assist can make your offer less attractive unless you increase the price to make up for it.

It’s a tool that works best when you understand the tradeoff between lowering your cash to close and staying competitive with the seller.

How Does Earnest Money Deposit Impact A Competitive Offer?

The earnest money deposit tells the seller one thing above all else: you’re serious.

How Can I Show Confidence through the Earnest Money Deposit?

Anyone can write a number on paper. Putting thousands of dollars into escrow shows commitment. Typically around 3% of the purchase price, the deposit signals confidence without immediately risking the funds.

The earnest money is protected by the contract as long as the buyers act in good faith. Most contracts allow you to walk away and keep your deposit if issues arise during inspections, title review, or financing. Where buyers get into trouble is when they simply change their mind without a valid contractual reason. If Title Can’t be cleared, you’re protected, and you’ll get your money back, but if you decide to move to Florida the day prior to closing, you might not be so lucky.

Understanding when your deposit is at risk—and when it isn’t—removes a lot of unnecessary fear.

Financing Terms

From a seller’s perspective, financing equals risk.

Why Do Sellers Care How You’re Paying?

Cash offers are strongest because they remove most uncertainty. Conventional loans generally come next, followed by FHA and VA loans, which tend to have stricter appraisal and property condition requirements.

This doesn’t mean FHA or VA buyers can’t compete—it just means sellers are weighing how likely the deal is to close without surprises. A well-prepared buyer with strong documentation and realistic expectations can offset financing concerns with clean terms elsewhere.

But even the best financing can fall apart if the home doesn’t appraise. That’s where understanding appraisal gaps becomes crucial.

How Do You Plan for Appraisals and Appraisal Gaps in Your Home Offer?

You offer $385,000 on a newly listed home in a hot neighborhood, and it gets accepted—but a week later, the appraisal comes in at $370,000.

Now what? Unless someone makes up the $15,000 difference, the deal could fall apart. That’s where understanding appraisal gap coverage becomes crucial.

Smart buyers think about this before submitting an offer. Reviewing comps gives a strong indication of likely appraised value, but appraisals are still subjective. In competitive markets, appraisal gap coverage can strengthen an offer—but it should never be added casually.

Sometimes the better move is a conversation with the listing agent upfront to set expectations, rather than committing to a gap that could stretch finances later.

How Important are Inspections in Your Home Buying Offer?

Inspections aren’t about finding a perfect house. They’re about understanding what you’re buying. Even brand-new homes can have issues hiding behind walls, under floors, or inside systems you can’t fully evaluate during a showing.

How do Inspections Really Impact a Strong Home Offer?

An inspection gives buyers the opportunity to hire a professional home inspector to take a closer look at the home’s major components, like the roof, foundation, plumbing, electrical, and mechanical systems.

First-time buyers often expect inspections to come back “clean.” In reality, nearly every home has findings. That’s normal. The goal isn’t zero issues; it’s understanding which problems are serious health & safety issues, which are maintenance-related, and which are manageable over time.

When buyers go into inspections with the right expectations, the process becomes far less stressful and much more useful.

Most buyers typically elect for a standard home inspection (structure, roof, plumbing, electrical, HVAC), and depending on the property, may add a few common supplemental inspections, such as:

- Termite inspection

- Radon testing

- Sewer line inspection (especially for older homes)

There are also inspections that are less common and usually only recommended when there’s a specific reason or concern, including:

- Mold inspection

- Stucco or exterior envelope inspection

- Well water and septic inspections

- Chimney or fireplace inspections

- Environmental or specialty inspections

Which inspections make sense depends on the home, the location, and the buyer’s comfort level. This is where guidance matters. Choosing the right inspections helps buyers stay protected without overcomplicating the process or weakening their offer unnecessarily.

Standard home inspections aren’t the only type buyers need to consider. In competitive situations—especially when you're trying to make your offer stand out—your agent may bring up something less familiar: the Use & Occupancy inspection.

When does a Usage & Occupancy Inspection become a contingency?

You’re under contract on a home just in Delaware County, when your agent says the township needs a Use & Occupancy inspection before closing.

It’s not part of your standard home inspection, and the seller looks relieved when you offer to take it on. Why? Because agreeing to handle U&O can actually strengthen your offer.

This is a township-issued inspection that confirms the property meets local safety and code requirements, and it’s completely separate from your home inspection.

Every township handles U&O differently, with its own timelines, fees, and repair standards, which can make it an extra hurdle for sellers.

Because of the varied requirements, taking responsibility for the U&O can actually strengthen your offer. When a buyer agrees to handle the U&O process, it saves the seller time, coordination, and potential stress, especially if minor repairs or follow-up inspections are required.

From the seller’s perspective, that’s one less task to manage before closing, which can make your offer feel smoother and easier to accept.

It’s important for buyers to understand what they’re agreeing to. A U&O inspection may require simple fixes, like installing handrails or updating smoke detectors, but in some cases it can involve more work depending on the township and the property.

That’s why this term works best when it’s discussed upfront with your agent. When used intentionally, taking on the U&O can be a smart way to stand out, especially in competitive markets, without having to raise your price.

How Closing Timelines Matter in Your Home Buying Offer?

Sellers often care about timing more than buyers expect.

How meaningful are Closing Timelines to a Strong Offer?

A flexible settlement date or possession agreement can sometimes matter more than an extra few thousand dollars in price, because timing directly affects the seller’s next move.

Some sellers want to close as quickly as possible to avoid another mortgage payment, while others need more time to find a new home, coordinate a move, or line up a lease. When a buyer can adjust their timeline—even slightly—it can make an offer feel easier and less stressful for the seller to accept.

Possession terms are part of this same conversation. Whether the seller needs post-settlement possession, early occupancy, or a rent-back period, being open to reasonable solutions can strengthen an offer without costing the buyer much financially. In competitive situations, flexibility here can be the difference between winning and losing, even if the price is similar to other offers.

Buyers also frequently overlook inclusions, which can create frustration later if they aren’t clearly spelled out. Appliances, fixtures, and personal property should never be assumed to stay.

Something as simple as a washer, dryer, refrigerator, or even light fixtures can become a problem if expectations aren’t aligned upfront. Clear language in the contract avoids last-minute surprises, awkward negotiations before closing, and post-settlement headaches.

Taking the time to confirm what’s staying, what’s going, and what must be removed helps ensure that closing day feels like a finish line.

Once you’ve addressed price, timeline, and financing, the next layer of strategy is understanding how the contingencies impact your offer’s strength.

How do Contingencies Work in Real Time? (Strength vs. Protection Is Always a Tradeoff)

In competitive situations, sellers are looking for clean, low-risk offers—and that often means reducing or waiving certain protections. But each contingency serves a purpose. Waiving one might make your offer more appealing, but it also exposes you to more risk.

That’s why it helps to think about contingencies not just as yes-or-no decisions, but as part of a broader strategy. Depending on the property and market, some contingencies may be negotiable—while others are critical to protect your investment.

Here's a breakdown of how each major offer element can include a built-in contingency, and how adjusting it affects the strength of your offer:

| Offer Element | Contingency / Protection | How It Protects You | How It Impacts Your Offer |

| Price | Appraisal Contingency | Ensures the home appraises at or near the offer price, or you can renegotiate or walk away | Shows you’re willing to bridge a financial gap if the appraisal comes in low—a big win for sellers |

| Earnest Money | Contractual exit clauses | Lets you reclaim your deposit if the deal falls apart under valid reasons (e.g., title, financing, inspection) | A higher deposit with fewer exit points signals strong intent and reduces seller uncertainty. |

| Inspections | Home inspection contingency | Allows you to back out or negotiate if serious issues are found | Waiving or limiting inspections removes hurdles for the seller and shortens their timeline. |

| Financing | Mortgage contingency | Lets you cancel without penalty if financing falls through | Protects you from any unforeseen issues during the final approval stages of your mortgage. |

| Closing Date | Flexibility (informal) | Protects your moving timeline and planning | Offering the seller a flexible settlement or rent-back can be more valuable than a higher price. |

These are just a few examples of how contingencies can be used strategically—not just as protections, but as tools to craft a stronger offer. A knowledgeable agent will help you evaluate which levers to pull, and when, based on your goals, your comfort level, and what matters most to the seller.

What Should I Think About Before Signing a Home Offer?

Before submitting an offer, your agent should walk you through every element of the contract in plain language, no jargon, no guesswork.

If you haven’t had that conversation yet, start here: What to Expect at Your Buyer Consultation; this is where we break down how your agent prepares you for writing an offer before you’re under pressure.

At a minimum, the offer conversation should answer four key questions:

- What are you offering, and what does that mean for your monthly payment?

- How much cash will you need to bring to the table at closing?

- When and how can you safely exit the deal if something unexpected comes up?

- What could realistically go wrong, and what happens if it does?

When buyers clearly understand the answers to these questions, the process stops feeling rushed and starts feeling strategic.

That’s exactly what the agents on our team are trained to do. We walk you through each part of the offer step by step, so you’re never left guessing. You’ll have the information, context, and market insight you need to make the best decisions for your situation. From there, we can draft a clean, confident, and competitive offer that reflects both your goals and what the seller is likely to value most.

Your Next Step In Preparing Your Home Offer

By now, you understand that a strong home offer is about more than just picking the highest price. It’s a complete strategy that balances risk, timing, and terms with what matters most to the seller.

Most buyers start this process feeling unsure, especially when they’re looking at a real estate contract for the first time. That confusion can lead to rushed decisions, costly mistakes, or missed opportunities.

Your next move is simple: schedule a time to walk through a sample offer with your real estate agent. Go over the terms, ask questions, and talk through different scenarios—before you're in a pressure-filled situation with real money on the line.

We’ve helped hundreds of Greater Philadelphia buyers navigate this exact process with clarity and confidence. When the time comes, we’ll help you submit an offer that protects your investment and puts you in the strongest position possible.

Robin Martin

Realtor® | Premier Home Team | Keller Williams Empower | PLACE

or another way