Categories

Home Buying Tips, Home OwnersPublished March 16, 2026

Renting vs. Buying a Home in Philadelphia

.jpg)

Renting vs. Buying in Philadelphia: What to Consider

Are you currently renting in Philadelphia and wondering whether it finally makes sense to buy?

With rising rents, unpredictable home prices, and everyone offering different advice — how do you know what’s truly right for you?

Here’s the truth most realtors don’t tell you: there’s no one-size-fits-all answer — and most advice you’ll hear oversimplifies the decision. The rent-versus-buy decision depends far less on headlines or rules of thumb and far more on your timeline, your lifestyle, and your long-term goals. For some people, renting is the smarter move right now. For others, buying sooner than expected can quietly change their financial trajectory.

In this guide, we’ll show you how to confidently compare the rent vs. buy scenario based on your timeline, monthly costs, equity potential, lifestyle, and local loan options.

At Premier Home we've helped over 250 Philadelphia renters explore this decision in 2026 alone. By the end of this article, you'll learn:

- How long you need to stay in Philly for Buying to Make Sense

- Why does the Renting vs Buying decision matter so early

- When does Renting actually make more sense

- What are the signs you might be ready to buy a home in Philadelphia

- How rising rents compare to a fixed mortgage payments

- Surprising costs for first time buyers in Philadelphia

- How to plan for maintenance on your Philly home

- If you really need 20% down to buy in Philly

- What questions should guide the renting vs buying decision

- The most common mistake first time buyers make

.jpeg)

How Long Do You Need to Stay in Philly for Buying to Make Sense?

Before comparing costs or loan options, the most important place to start is your timeline.

If you expect to move again in less than three years, renting often makes more sense financially. Short stays don’t usually give you enough time to offset closing costs or benefit from appreciation.

Once you’re planning to stay longer than three years, buying tends to tilt in your favor. That’s when principal payments and appreciation start working for you instead of against you.

This is why there’s no universal rule like “you must stay five years.” In many Philadelphia neighborhoods, buyers can break even — or better — in closer to three years depending on location and market movement.

Why does the Rent vs. Buy Choice Matter So Early?

Early in your financial life, decisions compound.

Renting gives you flexibility, but every monthly payment is gone forever. You don’t get it back. You don’t reuse it. It simply disappears.

Buying is different. Even when the monthly payment feels similar, part of what you’re paying each month becomes equity in your home, and that equity stays tied to your home - something you own.

Over time, that equity can be used to:

- Fund your next move

- Pay off student loans or other debt

- Make improvements without draining savings

- Build long-term financial stability

When people understand that they’re essentially “paying themselves back” over time, the conversation around buying shifts dramatically.

When Does Renting Actually Make More Sense?

Renting isn’t a bad choice, in fact, it’s the right choice in certain situations.

Renting usually makes sense if you expect a job or career change soon, aren’t sure where in the city you want to live, value flexibility over stability right now, or know your lifestyle will change in the next few years.

Philadelphia has many neighborhoods filled with young professionals (like Graduate Hospital & Fitler Square), active nightlife (like Fishtown & Northern Liberties), and renters with shorter-term living patterns (like Manayunk). For people who value flexibility or anticipate a lifestyle or employment change in the near future, renting can be a smart move while they figure out their next chapter.

The key is intentional renting. Have a plan for the next few years, and once your bigger picture, vision, and goals become clearer, revisit the option to buy.

Once you’ve thought about how long you’re staying, it’s time to look at other readiness signs.

What are the Signs You Might Be Ready to Buy a Home in Philadelphia?

Financial readiness often shows up before people realize it.

One of the clearest signs? Your rent payment already matches what a mortgage would cost. In many Philadelphia neighborhoods, renters paying $1,800–$2,200 per month are already in first-time buyer territory.

Emotional readiness matters too. Many renters decide to buy after:

- Dealing with repeated rent increases

- Having poor landlord experiences

- Wanting control over repairs and upgrades

- Feeling “stuck” despite being responsible tenants

In these cases, buying often becomes less about math and more about gaining control over your living situation.

.jpg)

How do Rising Rents Compare to Fixed Mortgage Payments in Philadelphia?

This is where zooming out changes everything.

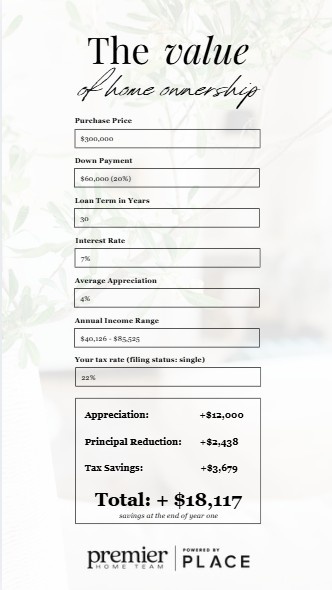

If you’re paying $1,500 per month in rent, that adds up to $18,000 per year — or $90,000 over five years. Once renters see those numbers laid out, the conversation often shifts. That money is gone, with no equity, no appreciation, and nothing to reuse later.

What $1,500/month Looks Like Over 5 Years Renting vs Buying

| Year |

Total Rent Paid (Renting) |

Mortgage Paid (Buying) |

Estimated Equity Gained (Buying) |

| 1 |

$18,000 |

$18,000 |

$3,000 |

| 2 |

$36,600 |

$36,000 |

$8,000 |

| 3 |

$55,800 |

$54,000 |

$14,000 |

| 4 |

$76,200 |

$72,000 |

$21,000 |

| 5 |

$97,800

|

$90,000

|

$30,000

|

Note: Mortgage payments include both principal and interest; equity estimates assume modest appreciation and average loan terms.

Over 5 years, renters pay nearly $100,000 with nothing to show for it — while buyers build $30,000+ in equity on average.

One of the biggest frustrations renters share in Philadelphia is year-over-year rent increases. It’s common to see rents rise by $100 or more each year, regardless of whether income increases at the same pace. Over time, that rising cost eats into savings and limits flexibility.

With a mortgage, those same monthly payments are different. While not every dollar builds equity immediately, a meaningful portion goes toward principal, and appreciation adds another layer of long-term value. Instead of paying more each year for the same space, you’re gradually building ownership in something that can benefit you later.

Mortgage payments are also largely fixed. While property taxes and insurance can change, your core payment stays stable. Locking in today’s cost of living creates predictability — and predictability creates breathing room to save, invest, and plan for the future.

Surprising Costs for First-Time Homebuyers in Philadelphia

Upfront, buyers are often surprised by closing costs — mostly because they don’t understand what they are.

Clear explanations of closing costs can make a huge difference. When buyers understand these additional costs, and see where each dollar goes (taxes, escrow, title, transfer fees), anxiety drops.

After closing, a few things can catch first-time buyers off guard — not because they’re problems, but because no one warned them ahead of time.

One common surprise is loan servicing transfers. Many mortgage lenders sell the servicing rights shortly after closing, which means your loan didn’t change — but who you send your payment to did. It can feel jarring when you’re still getting used to homeownership, but it’s routine and doesn’t affect your rate or terms.

Another surprise is the sudden flood of junk mail and scam solicitations. New homeowners are often targeted with official-looking letters asking for payments, insurance add-ons, or warranty fees. Most of these are marketing or outright scams. Knowing this ahead of time makes it much easier to spot what’s legitimate and what can be ignored.

Finally, some buyers experience insurance or property tax adjustments during the first year. Insurance premiums can change, and property taxes may be reassessed after purchase, which can slightly impact your monthly payment. These adjustments are normal — and manageable — once you understand why they happen and how to plan for them.

None of these are deal-breakers. They’re simply part of the transition from renting to owning — and they’re far easier to handle when you know what to expect and have the right guidance in place.

.jpg)

How do you Plan for Maintenance on Your Philly Home?

Owning a home does come with more responsibility. The shift from “nothing is my problem” to “everything is my problem” can feel abrupt, especially for first-time buyers who are used to calling a landlord when something breaks.

This is exactly why home inspections matter so much. A quality inspection doesn’t just look for issues — it gives buyers a roadmap for ownership. It helps you understand what needs attention right away, what’s likely coming in the next few years, and what major systems should be fine for the long term.

Understanding the expected lifespan of big-ticket items like the roof, HVAC system, plumbing, and electrical allows buyers to plan instead of react. When you know, for example, that a water heater may need replacement in a few years or that a roof has a decade of life left, those future costs become manageable — not emergencies.

Planning for maintenance isn’t about expecting problems. It’s about being informed and prepared, so small issues don’t turn into expensive surprises. With the right inspection and a basic understanding of what you’re responsible for, the transition from renting to owning feels far more manageable — and far less intimidating.

Do You Really Need 20% Down to Buy in Philly?

One of the biggest misconceptions keeping renters stuck is the belief that you need a 20% down payment to get started with homeownership. That assumption alone causes many capable buyers to delay the process for years longer than necessary.

In reality, many loan options allow buyers to put down as little as 3% to 3.5%, depending on the loan type and qualifications. On top of that, experienced agents can help buyers identify first-time homebuyer grants and assistance programs that further reduce upfront costs, sometimes covering a portion of the down payment or closing expenses.

Because of these options, many Philadelphia buyers are genuinely surprised to learn they can purchase a home with less than five figures out of pocket, even at higher price points. Once the barrier to entry feels more realistic, the conversation often shifts from “someday” to “sooner than I thought.”

Comparing Upfront Costs vs Long Terms Value - Renting vs. Buying a 3 Bedroom Townhome in Glenolden, PA

| Rent |

Buy |

||

| Avg rental Rate: |

$2,000/mth |

Average Purchase price: |

$250,000 |

| Initial Out of pocket: (first/last/sec): |

$6,000 |

Cost to purchase (CC and DP FHA): |

$21,768 |

| Average Term: 12 months |

Mortgage amount: |

$1,880.00 |

|

| Average increase: $75/year |

Down Payment: |

$8,750.00 |

|

| Total Spent after 1 year: |

$26,000 |

Total spent year 1 (CC and Mortgage Payments): |

$44,328 |

| Total Year 1+2 (With increase): |

$50,900 |

Principal paid year 1: |

$2,693 |

| Total Year 1-3 (With increase): |

$76,700 |

EOY1 Net worth (principal payments and DP) : |

$11,433 |

| Total Year 1-5 (With increase): |

$131,000 |

EOY2 Net worth (PP, DP, and 2% appreciation): |

$19,317 |

| EOY3 Net worth (PP, DP, and 2% appreciation): |

$27,483 |

||

| EOY4 Net worth (PP, DP, and 2% appreciation): |

$35,957 |

||

| EOY5 Net worth (PP, DP, and 2% appreciation): |

$44,651 |

||

| End of 5 year total spend: |

$131,000 |

End of 5 year total spend (mortgage and CC): |

$129,768 |

| Net worth gain after 5 years of ownership: |

$44,651 |

||

| Total spent less than net worth gain: |

$85,117 |

Comparing Upfront Costs vs Long Terms Value - Renting vs. Buying a 3 Bedroom Townhome in Cobbs Creek, PA

| Avg rental Rate: |

$1,800 |

Average Purchase price: |

$225,000 |

| Initial Out of pocket: (first/last/sec): |

$5,200 |

Cost to purchase (CC and DP FHA): |

$22,348 |

| Average Term: 12 months |

Mortgage amount: |

$1,760 |

|

| Average increase: $50/year |

Down Payment: |

$7,875 |

|

| Total Spent after 1 year: |

$23,400 |

Total spent year 1 (CC and Mortgage Payments): |

$43,468 |

| Total Year 1+2 (With increase): |

$45,600 |

Principal paid year 1: |

$2,425 |

| Total Year 1-3 (With increase): |

$68,400 |

EOY1 Net worth (principal payments and DP) : |

$10,300 |

| Total Year 1-5 (With increase): |

$115,400 |

EOY2 Net worth (PP, DP, and 2% appreciation): |

$17,388 |

| EOY3 Net worth (PP, DP, and 2% appreciation): |

$24,739 |

||

| EOY4 Net worth (PP, DP, and 2% appreciation): |

$32,367 |

||

| EOY5 Net worth (PP, DP, and 2% appreciation): |

$40,192 |

||

| End of 5 year total spend: |

$115,400 |

End of 5 year total spend (mortgage and CC): |

$127,948 |

| Net worth gain after 5 years of ownership: |

$40,192 |

||

| Total spent less than net worth gain: |

$87,756 |

Renting may cost less upfront, but buying offers long-term value that grows over time — through equity and appreciation.

What Questions Should Guide the Rent vs. Buy Decision?

Before choosing rent or buy, ask yourself:

- How stable is my career location, not just my job?

- Do I want flexibility or predictability right now?

- Am I planning for a family in the next few years?

- Will pets, space, or schools matter more soon?

Sometimes renting fits now, but buying fits the future you’re already planning for.

What is the Most Common Mistake First-Time Buyers Make?

The most common mistake we see is buyers telling themselves, “I’ll just rent for one more year.” It feels safe, low-risk, and easy to justify — especially when buying still feels intimidating.

But one year often turns into five. And during that time, you may miss out on years of equity, appreciation, and stability you could already have working in your favor. Instead of building something you own, those payments continue going toward rent with nothing to show for them down the line.

That doesn’t mean everyone should rush into buying. It simply means that waiting by default — rather than making an informed decision — can quietly become one of the most expensive choices first-time buyers make.

What’s the Most Obvious Low-Pressure Next Step?

Now that you understand how timelines, equity, loan options, and rising rents all factor into the decision, you’re in a much better place to make a confident next move.

If you’ve been renting in Philadelphia and feeling unsure about buying, you’re not alone. It’s normal to feel stuck between rising rents and the fear of making the wrong choice.

The most helpful next step isn’t deciding today — it’s getting clarity. Sitting down with a knowledgeable local professional, without pressure, helps you see what your real options are and what makes the most sense for your lifestyle and budget.

That’s exactly what our team does - we’ve helped hundreds of Philly renters map this out, and we’d be happy to help you get the answers you need — so you can move forward with confidence.

👉 Schedule a consultation to explore whether renting or buying makes the most sense for you. No pressure. Just clear answers, honest guidance, and a better understanding of your next move.

|

or another way