Categories

Home Buying TipsPublished June 17, 2026

Do I Qualify for First-Time Home Buyer Programs in Philadelphia?

You’ve done the math. You’ve checked your savings. And now you’re staring at a screen wondering: “Is there money out there to help me buy my first home, and do I actually qualify for it?”

That question trips up a lot of first-time buyers in the Philadelphia area. Some assume they won’t qualify because they think their income is too low, or because they once owned a home. Others miss out entirely because they never asked. And a few discover, too late, that the programs they were counting on didn’t apply to the county they were shopping in.

At Premier Home Team, we’ve walked buyers through this process across Philly and the surrounding suburbs. We’ve seen clients save $10,000 or more by qualifying for programs they didn’t even know they were eligible for. We’ve also seen buyers waste months chasing the wrong information online when a single phone call would have cleared everything up.

This article is going to give you a straight answer on what first-time home buyer programs actually look for. We’ll cover your first-time buyer status, income limits, credit score, price point, and the mistakes that knock people out of contention. By the end, you’ll know where you stand, and exactly what to do next.

If you’re still trying to understand how down payment assistance programs actually work — including grants, forgivable loans, and repayment structures — read our guide: What Is Down Payment Assistance and How Does It Work?

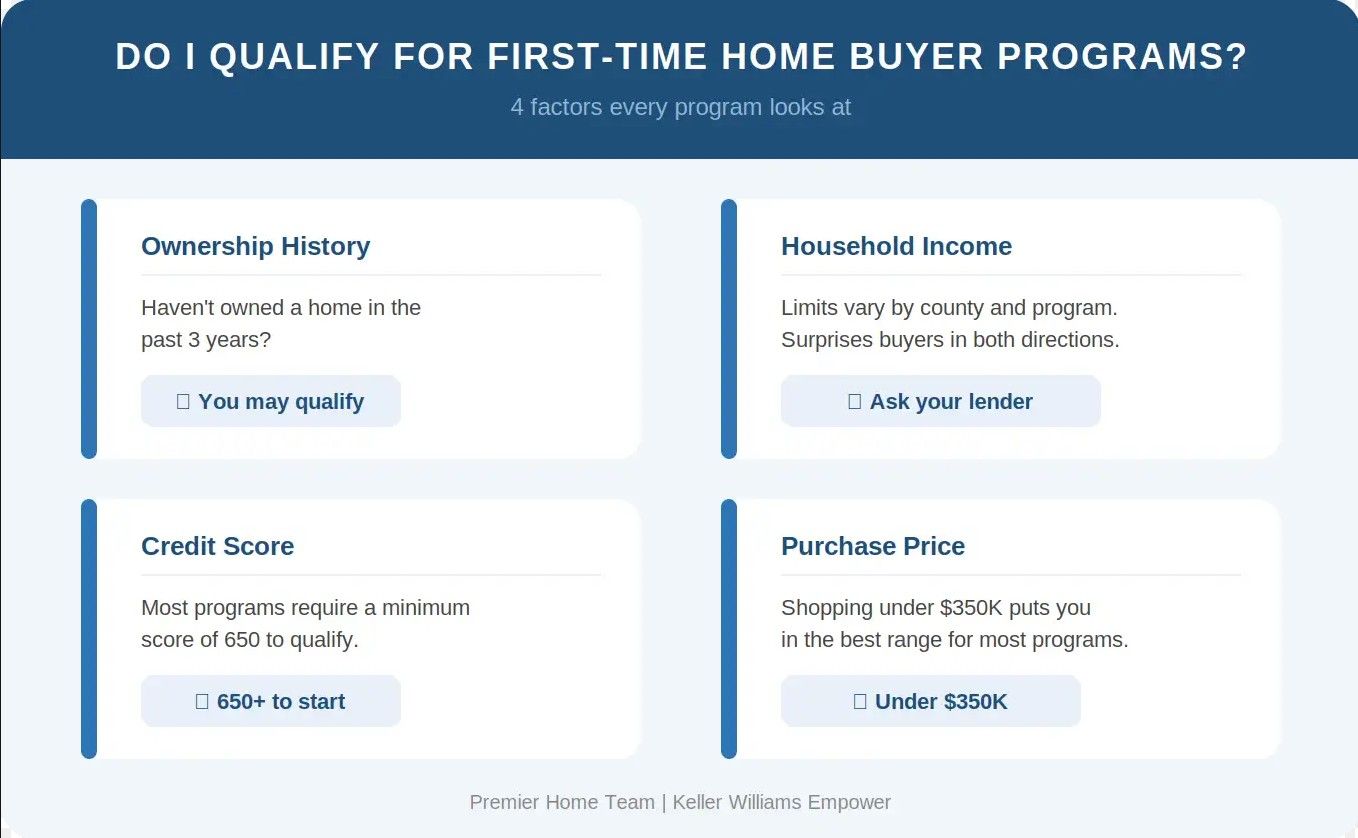

What Does “First-Time Home Buyer” Actually Mean?

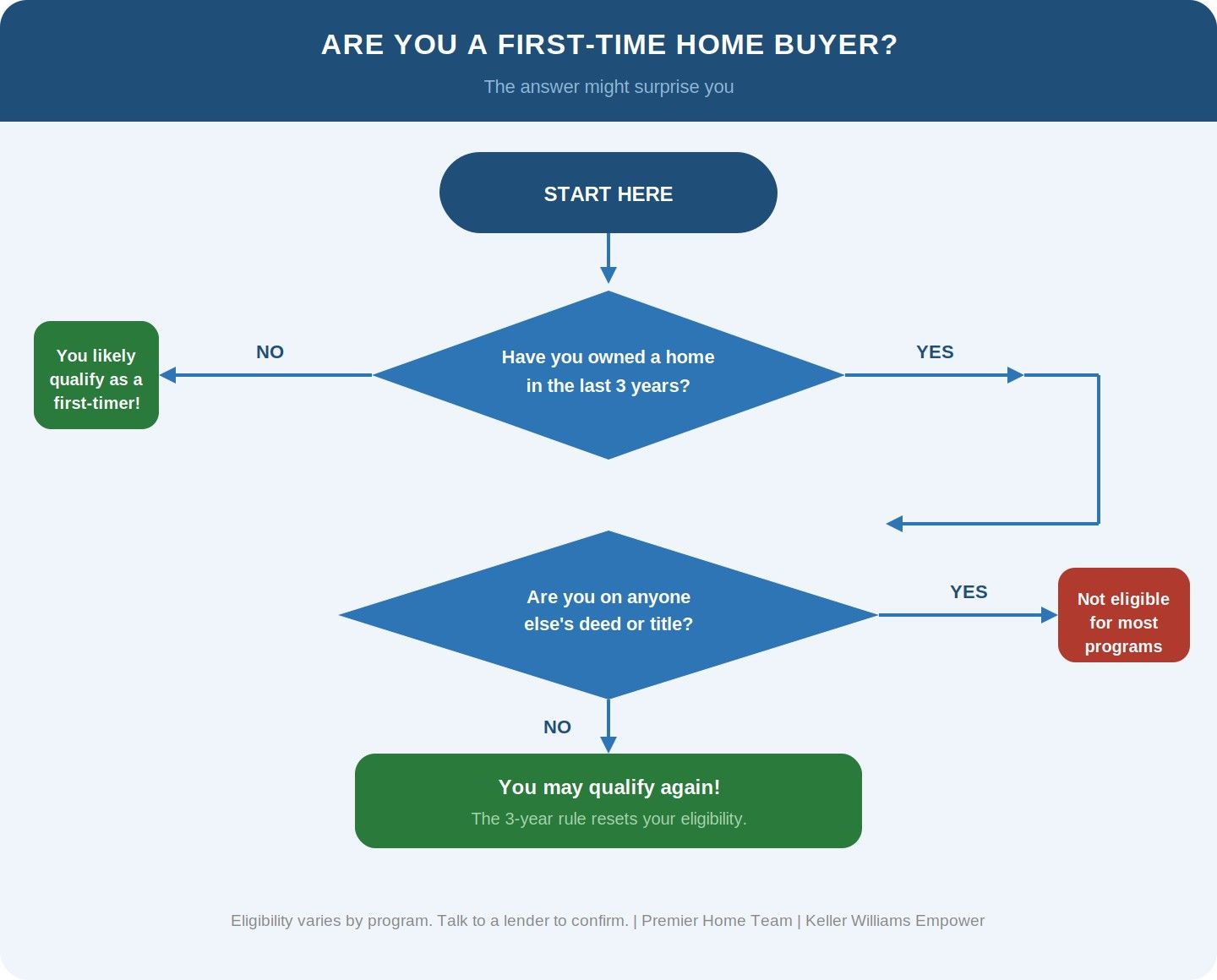

Most people assume the answer is obvious: if you’ve never bought a home, you qualify. But per HUD’s definition of a first-time home buyer, the rule is broader than most people expect, and it works in your favor more often than you’d think.

A “first-time home buyer” is anyone who has not owned a home in the past three years. That’s it. So if you bought a home, sold it, and have been renting for the last four years, you can qualify. Joe has seen this play out firsthand:

“I had a client who bought and sold a home seven years prior. When I asked if he’d ever owned before, he said yes, and he automatically assumed that excluded him permanently. Once I explained the three-year rule, he qualified for a program that saved him $10,000 toward closing costs. That money stayed in his pocket to furnish the place the way he wanted.”

One Ownership Issue That Can Disqualify You

Being on someone else’s deed, even for inheritance purposes or power of attorney, counts as ownership in the eyes of these programs. If your name is on any deed, anywhere, you’re not going to qualify. The programs don’t leave room for interpretation on that one.

First-Time Home Buyer Income Limits: What Surprises Most Buyers

Income limits are where things get tricky. Every program has a threshold, and whether you’re buying alone or with a partner affects how that number is calculated.

What surprises most people? They often make too much money to qualify, not too little. If your household income is on the higher end, you may find yourself just above the cutoff for many programs, especially in the suburbs.

The other thing to know: income limits are not universal. They vary significantly from city to county to program. A program available in Philadelphia proper may not apply in Chester County or Montgomery County. Programs are typically non-transferable across county lines.

The clearest way to find out where you stand? Don’t rely solely on what you read online. You can browse statewide options through the Pennsylvania Housing Finance Agency, but for county-specific limits, call the program directly or sit down with a lender who knows the local landscape. You’ll get a much clearer answer in minutes instead of spending hours going down the wrong rabbit hole.

Credit Score and Financial Profile Requirements for Down Payment Assistance

Most programs use 650 as the baseline credit score. If you’re above that, you’re in good shape for most programs’ eligibility criteria. Below 650, your options narrow significantly. It’s rare to find programs willing to work with lower scores.

Credit score is the single biggest barrier we see. Before you do anything else, check your credit score before you apply. It's free, it won't hurt your score, and it tells you exactly where you stand before you walk into a lender's office.

Beyond credit score, programs also look at your debt-to-income ratio (DTI) to make sure you can handle not just the assistance, but what you need to qualify for a mortgage. Student loans factor in, too, though the way they’re calculated in your DTI is more nuanced than most buyers realize. Lenders don’t weigh the full balance against you the way you might expect.

There’s also a less obvious factor: reserve funds. Programs want to see that you’ll have some cushion left after closing. At the same time, certain assistance programs may limit how much liquid savings you can have and still qualify for assistance.

The important thing to understand is that qualification isn’t based on one number alone. Credit score, debt, savings, income, and purchase price all work together, which is why two buyers with similar incomes can end up with very different eligibility outcomes.

How Purchase Price Affects Your Eligibility for First-Time Buyer Grants

Price point is another eligibility signal. As a general rule of thumb, buyers shopping above $400,000 are much less likely to qualify for first-time home buyer assistance programs. If you’re in the $200,000–$350,000 range, you’re in the zone where eligibility becomes a much more realistic conversation.

Some programs are percentage-based, meaning the higher the purchase price, the larger the potential assistance amount. But higher price points also tend to come with higher household incomes, which can quickly push buyers over a program’s income limits.

Purchase price also affects the types of homes and areas buyers are targeting. A buyer shopping in Philadelphia proper may qualify for programs that wouldn’t apply to a similar-priced home in the surrounding suburbs, where pricing and income thresholds often look very different.

That’s why the purchase price can’t really be evaluated on its own. The home price, your income, the county you’re buying in, and the program guidelines all work together to determine whether you qualify.

Common Reasons Buyers Don’t Qualify, And How to Fix Them

A lot of buyers are closer to qualifying than they realize, but their credit profile is usually the thing holding them back. Many of these buyers just haven’t had visibility into where their credit stands, or what it would take to get it there. Getting that number and making a plan is step one.

Ownership issues catch people off guard too. If you co-signed on a property for a family member, inherited a home, or were added to a deed for estate planning reasons, that can affect your eligibility even if you never considered yourself a homeowner.

Another common mistake is assuming you don’t qualify without ever checking. Buyers often rule themselves out because of something they read online or because they assume these programs are only for low-income buyers. In reality, eligibility varies widely depending on the program, the county, and your overall financial picture.

The buyers who usually have the best outcomes are the ones who start the conversation early. Even if you’re not quite ready today, understanding where you stand now gives you time to improve the areas that matter most before you’re actively house hunting.

What to Do If You’re Close But Not Quite There Yet

Patience is part of this process. If your credit score needs improvement or your income is slightly outside a program’s limits, that doesn’t necessarily mean homeownership is off the table. More often, it means you need a plan and a realistic timeline.

The buyers who make the most progress are usually the ones who start preparing before they’re under pressure to buy immediately. Even small financial improvements over the course of three to six months can change what programs, loan options, or price ranges become available to you.

The most effective next steps are usually pretty straightforward:

- Review your full financial picture so you understand where your biggest opportunities for improvement are.

- Focus on the changes that will have the biggest impact, whether that’s paying down debt, improving your credit, or adjusting your target price range.

- Research the areas you want to buy in so you understand how pricing and program availability may differ from county to county.

- Stay consistent. Buyers who check in periodically and keep moving forward tend to have far more options when they’re finally ready to purchase.

A lot can change in a relatively short amount of time. Buyers who don’t qualify today are often surprised by how different their options look six months later with the right preparation.

How First-Time Buyer Assistance Affects Your Offer

When you’re writing an offer using a down payment assistance program, you’ll need to disclose that to the seller upfront. Some programs come with additional inspection or repair requirements, and a seller who wasn’t prepared for that can push back. Transparency from the start prevents that conflict.

One more note: some programs can be paired with seller’s assist, another tool that keeps more money in your pocket at closing. They’re not directly connected, but structuring your offer correctly can make both work together. That’s a conversation worth having with your agent early.

Your Next Step Toward Buying Your First Home in Philadelphia

Qualifying for a first-time home buyer program in the Philadelphia area comes down to a few clear factors: your ownership history over the past three years, your household income relative to the program’s limits, your credit score, and the price range you’re shopping in.

If you’ve been sitting on this question, wondering whether there’s money available to help you get into your first home, there’s a good chance programs exist that could help. These programs exist for a reason, and the buyers who use them aren’t weaker buyers. They’re the smarter ones.

At Premier Home Team, we work with buyers across Philadelphia and the surrounding suburbs every day. We know which programs are available, how they work with your offer, and how to position you as a competitive buyer even when you’re using assistance.

Ready to see what's available where you're shopping? We've put together county-by-county breakdowns of the programs in your area:

- First-Time Home Buyer Programs in Philadelphia County

- First-Time Home Buyer Programs in Delaware County

- First-Time Home Buyer Programs in Montgomery County

- First-Time Home Buyer Programs in Chester County

- First-Time Home Buyer Programs in Bucks County

Find your county and see what programs may apply to your situation. And if you want someone to walk you through your options, schedule a buyer consultation with our team and we'll take it from there.\

Frequently Asked Questions About First-Time Home Buyer Program Eligibility

Can I qualify if I owned a home in the past?

Yes. Most first-time home buyer programs use a three-year rule, meaning you may qualify again if you haven’t owned a home within the last three years.

What credit score do I need for first-time home buyer grants in Pennsylvania?

Many programs use 650 as a general benchmark, though requirements vary. Buyers with higher scores typically have more assistance options available to them.

Do income limits apply to both buyers if I’m purchasing with a partner?

Usually, yes. Most programs look at the combined household income of everyone on the loan when determining eligibility.

What happens if my purchase price is over the program’s limit?

If the home exceeds a program’s purchase price cap, you likely won’t qualify for that specific assistance program, even if the rest of your financial profile fits the guidelines.

Can I use seller’s assist along with a first-time home buyer grant?

In many cases, yes. Seller’s assist and down payment assistance programs are separate tools, but they can often be combined to reduce your upfront closing costs.

Do first-time home buyer programs apply in every county?

Some programs are available statewide, while others are specific to certain counties or cities. That means a first-time home buyer program available in Philadelphia County may have different income limits, assistance amounts, or eligibility requirements than a similar program in Bucks, Chester, Delaware, or Montgomery County.

|

or another way